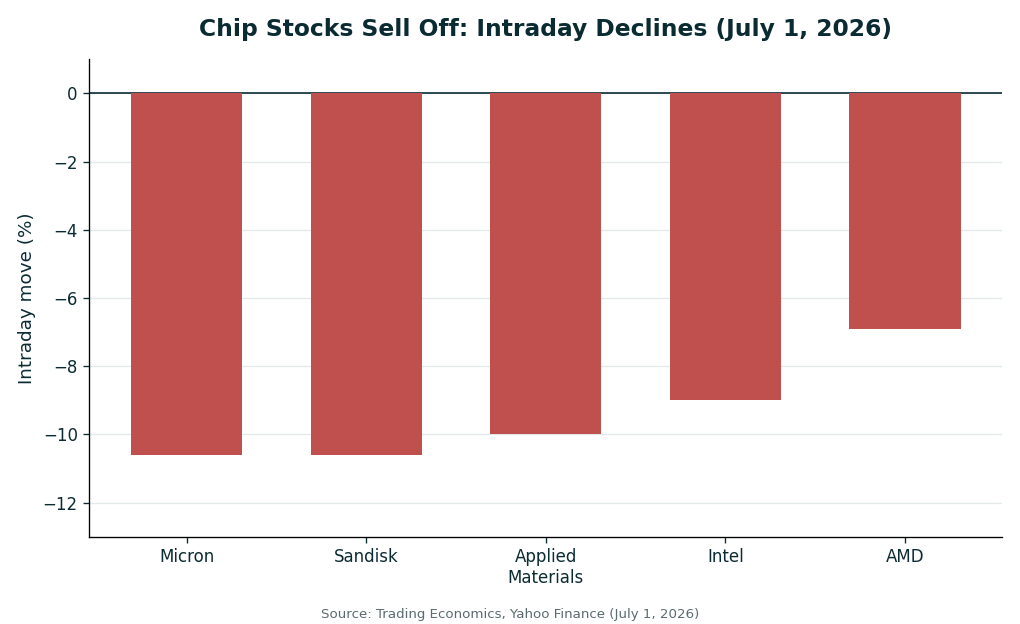

After a first half that felt unstoppable, the AI chip trade finally flinched. On July 1, 2026, semiconductor stocks sold off hard: Micron fell about 10.6%, Sandisk dropped a similar 10.6%, Applied Materials shed roughly 10%, Intel slid around 9%, and even AMD gave back close to 6.9%. Chip ETFs such as SMH and SOXX lost more than 5% in a single session. After parts of the sector rallied 70% to 100% this year, the question is blunt: is this a healthy pause, or the start of something worse?

The honest answer is that one red day cannot settle a debate this big. But the character of the selling who fell hardest, and why, tells you a great deal about what the market is actually worried about.

This Was Profit-Taking on the Market's Most Crowded Trade

The simplest explanation is usually the right one, and here it is profit-taking. Semiconductors were the defining trade of the first half of 2026. AI-driven demand pushed memory and accelerator names to record highs, and the sector became one of the most crowded positions in the entire market. When a trade gets that consensus, it does not take much, a hot economic print, a cautious analyst note, or simply the calendar turning into a new quarter to trigger a rush for the exits.

Notice the pattern in the declines. The steepest losses landed on the names that had run the furthest: memory makers like Micron and Sandisk, and equipment supplier Applied Materials. That is the signature of investors banking gains on their biggest winners, not of a market discovering a fundamental crack. The chart below shows just how concentrated the damage was.

Why Memory Names Like Micron Sit at the Center of the Storm

It is no accident that Micron was among the hardest hit. Memory has been the surprise star of the AI buildout, because high-bandwidth memory is the component that feeds data to the GPUs everyone talks about. That made Micron one of 2026's best performers and therefore one of the most exposed when traders decided to lock in gains. We laid out the bull case in detail in Micron's HBM Supercycle Could Redefine AI Growth, and nothing about a single down session changes that structural story.

The flip side of a great rally is a violent one. Stocks that triple do not give back their gains politely; they swing hard in both directions. The same leverage to AI demand that sent memory names soaring is exactly what makes them fall fastest when sentiment wobbles. High reward has always carried high volatility, and investors in this corner of the market signed up for both.

Why a 10% Drop Is Not the Same as a Bubble Bursting

Context matters enormously. A stock that has doubled or tripled in a year can fall 10% and still be up massively for 2026. That is not a collapse; it is a correction inside a powerful uptrend. Analysts covering the sector broadly framed the July 1 move as a healthy pullback rather than a reversal of the underlying AI-driven cycle. Corrections are how overheated trades cool without breaking, and they often set up the next leg by shaking out the weakest hands.

It is also worth remembering that chip earnings have, for the most part, backed up the enthusiasm. Even when individual reports disappointed on guidance, as we saw in AMD's Q4 earnings, where strong results still met a sharp stock drop, the demand backdrop for AI compute stayed intact. A market that punishes even good news is a market that has priced in a lot, but that is a valuation problem, not a demand problem.

The Counter-Argument (And Why It's Serious)

Here is the case that should keep bulls honest. Crowded trades do not just correct, sometimes they unwind, and the unwinds are brutal precisely because everyone owns the same thing. When positioning is this one-sided, a 10% down day can become the first domino rather than a buying opportunity. The bear argument is that AI infrastructure spending has run ahead of the actual, monetizable demand for AI services, and that at some point the companies writing the enormous checks will slow down. If hyperscaler capex plateaus, the memory and equipment names with the most operating leverage would feel it first and worst.

That concern is not paranoia; it is the central tension of this entire market. The counterpoint is that, so far, the spending commitments keep rising rather than falling, and demand for AI compute continues to outstrip supply in key components. A correction driven by positioning and profit-taking looks very different from one driven by collapsing orders, and the evidence on July 1 pointed to the former. The risk is real, but the trigger for the sell-off appears to be crowded positioning, not a fundamental break. The distinction is everything, and it is why the next data points matter so much.

The One Number to Watch

Forget the daily noise and watch one threshold: whether the major chip ETFs (SMH and SOXX) hold within roughly 20% of their 2026 highs. A pullback that stays shallower than that, after a 70%-plus run, is the textbook definition of a healthy correction. A decline that pushes past a 20% drawdown and keeps going would signal that the market has stopped taking profits and started repricing the whole AI-infrastructure thesis. That single line correction versus bear market, is the one worth tracking in the weeks ahead.

Frequently Asked Questions

Why did chip stocks sell off on July 1, 2026? Mainly profit-taking after a historic rally. Semiconductors were the market's most crowded trade in the first half of 2026, and traders locked in gains on the biggest winners, with memory names falling hardest.

How far did the major chip stocks fall? On the day, Micron and Sandisk each dropped about 10.6%, Applied Materials fell roughly 10%, Intel slid around 9%, and AMD declined close to 6.9%. Chip ETFs SMH and SOXX lost more than 5%.

Is this a correction or the start of a crash? Analysts broadly described it as a healthy correction within a longer-term uptrend rather than a reversal. After sector gains of 70%–100% in 2026, a single-digit-to-10% pullback keeps most names sharply higher for the year.

What is the biggest risk to chip stocks now? That AI infrastructure spending outpaces real demand and hyperscaler capex slows. The most leveraged names, memory and equipment makers would be the most exposed if that happened.

Disclaimer: Content on this site is for informational and educational purposes only and does not constitute financial, investment, or trading advice. I am not a licensed financial advisor. Always conduct your own research and consult a licensed professional before making investment decisions.