Picture this: your car won't start, the repair is $900, and payday is two weeks away. Do you reach for a credit card and pay it off slowly with interest, or do you calmly pull the money from savings? That difference is what an emergency fund buys you. It is simply a stash of cash set aside for life's surprises, kept somewhere safe and easy to reach. And here is the sobering part: a 2026 Bankrate survey found that only about 47% of Americans could cover a surprise $1,000 expense straight from savings. If you are one of the many who couldn't, you are not behind, you are exactly where this guide is meant to help.

What an Emergency Fund Actually Is (and Isn't)

An emergency fund is money reserved for true emergencies: a job loss, a medical bill, an urgent home or car repair. The key word is liquid, which just means you can turn it into spendable cash quickly, without penalties or waiting days. That rules out money locked in your retirement account or tied up in stocks that might be down when you need them.

It also isn't a vacation fund, a shopping cushion, or your everyday checking balance. Mixing those together is the classic trap: the money quietly gets spent, and the "emergency" fund isn't there when a real emergency arrives. Think of it as a financial airbag. You hope you never deploy it, but you would never drive without one.

How Much Should a Beginner Save?

The classic rule of thumb is three to six months of essential expenses. "Essential" means the bills you can't skip: rent or mortgage, utilities, groceries, insurance, minimum debt payments. If your must-pay costs are $2,500 a month, a three-month cushion is $7,500 and a six-month cushion is $15,000. That can feel enormous when you're starting from zero, so don't start there.

Start with a $1,000 starter goal, the exact expense nearly half of Americans said they couldn't cover. Once you clear that, aim for one month of expenses, then build toward three. Save whatever fits your life, whether that's $25 a week or $300 a month, and let consistency do the heavy lifting. People who are self-employed or have irregular income often aim for the higher end (six months or more), because their lean months are harder to predict.

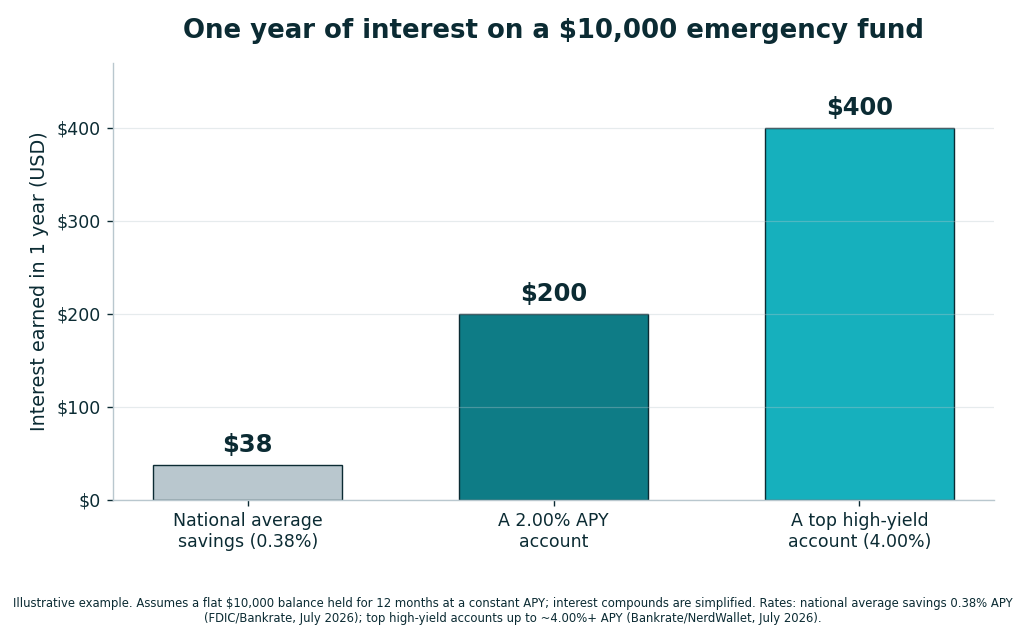

Where to Keep It: Why Today's Rates Matter

Here's where a lot of beginners lose money without realizing it. The average regular savings account in the U.S. pays a national average of about 0.38% APY as of mid-2026, according to Bankrate. APY stands for annual percentage yield, which is just the interest rate your money earns in a year, including the effect of compounding. By contrast, top high-yield savings accounts, which are ordinary, federally insured savings accounts that simply pay more, were advertising rates around 4.00% APY, and in some cases higher, in July 2026.

Why the gap? A high-yield account isn't riskier; the banks offering them are often online-only, so they pass their lower costs on to you. The chart below shows how much a flat $10,000 emergency fund would earn in interest over one year at different rates. It is an illustrative example, but the lesson is real: the account you choose can be the difference between earning about $38 and about $400 for doing nothing more than keeping your money in a smarter place.

One reason these high-yield rates exist at all is the Fed (the Federal Reserve, the U.S. central bank that sets a key interest rate). In mid-2026 the Fed held its benchmark rate at a range of about 3.50% to 3.75% to keep inflation in check, and when that rate is high, savings rates tend to stay attractive too. Rates won't stay this generous forever, which is a reason to put your emergency fund to work now rather than later. For a look at how to save after your cushion is built, see our guide below on retirement accounts.

Read: The Hard Truth About Maxing Out Your 401(k)

The Counter-Argument (And Why It's Serious)

Not everyone thinks a big pile of cash is smart. The strongest objection goes like this: cash loses value to inflation (the general rise in prices over time). If your savings earn 4% but prices rise 4%, your money isn't really growing, and consumer prices in 2026 sat roughly 26% higher than they were in late 2019. Meanwhile, money invested in the stock market has historically earned far more over the long run. So why let thousands of dollars sit "idle"?

It's a serious point, and here's the balanced answer: an emergency fund's job is not to grow your wealth, it's to protect you so you never have to sell investments at a bad time or borrow at 24% credit-card interest. The return on avoiding a high-interest debt spiral is huge and certain, while stock returns are neither guaranteed nor liquid on the day your roof leaks. A sensible middle path is to keep your emergency fund modest but real (three months for most people), park it in a high-yield account so it at least keeps pace with inflation, and invest the money beyond that cushion. You get safety and growth, in the right order.

The One Number to Watch

If you track just one number, make it your months of expenses covered: your emergency fund balance divided by your essential monthly costs. If you have $6,000 saved and spend $2,000 a month on essentials, you have three months of coverage. This single figure tells you more than a dollar amount ever could, because it's measured against your life, not someone else's. Watch it climb from zero, to one month, to three. Each step is a real reduction in how exposed you are to life's surprises, and a real increase in how well you sleep at night.

Read: Unexpected Expenses for Retirees: How to Plan and Save Smartly

Frequently Asked Questions

How fast should I build my emergency fund?

There's no single deadline. Focus first on a $1,000 starter cushion, then build toward one month, then three. Automating a small weekly or monthly transfer, even $25, keeps it growing without you having to think about it.

Is a high-yield savings account safe?

Reputable high-yield accounts held at banks covered by federal deposit insurance protect your balance up to the insured limit, just like a regular savings account. The main difference is a higher interest rate, not higher risk. Always confirm an account is federally insured before opening it.

Should I pay off debt or build savings first?

Many experts suggest doing a little of both: build a small $1,000 starter fund so a surprise doesn't push you deeper into debt, then throw extra money at high-interest debt, and return to fully funding your emergency savings afterward.

Where should I NOT keep my emergency fund?

Avoid places that are hard to access quickly or that can drop in value, such as retirement accounts (which carry penalties for early withdrawal), stocks, or crypto. The whole point is money you can reach instantly, at full value, on your worst day.

Disclaimer: Content on this site is for informational and educational purposes only and does not constitute financial, investment, or trading advice. I am not a licensed financial advisor. Always conduct your own research and consult a licensed professional before making investment decisions.