Here is a puzzle that trips up almost every new investor. On Thursday, Taiwan Semiconductor (TSMC), the company that makes the most advanced chips on Earth reported the best quarter in its history. Profit jumped a record 77%. And the stock fell about 3-4%. If the company just crushed it, why did shares go down? That question is one of the most useful lessons a beginner can learn, and TSMC is the perfect stock to watch while learning it. Let's break down what happened, why the market shrugged, and what to keep an eye on. This is educational, not a recommendation to buy.

First, What Does TSMC Actually Do?

Most tech giants design their chips but don't build them. TSMC is the world's largest "foundry" a contract factory that manufactures chips for other companies. When Apple, Nvidia, or AMD design a processor, TSMC is usually the one that physically produces it. That makes TSMC the quiet backbone of the entire technology world, and especially of the AI boom: if you've heard that Nvidia's chips power AI, remember that TSMC is the company actually making them.

Because it sits at the center of everything, TSMC's results are treated as a health check for the whole chip industry. When TSMC talks, the market listens.

The Record Numbers

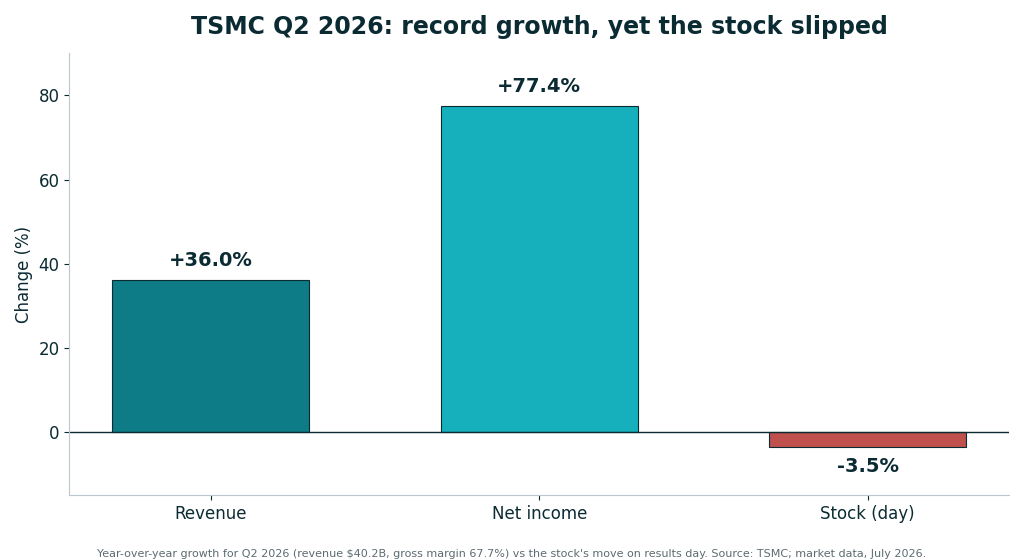

TSMC's second-quarter 2026 results were genuinely excellent:

- Revenue: about $40.2 billion, up 36% from a year earlier

- Net income (profit): up a record 77.4% year over year

- Gross margin: a fat 67.7% meaning it keeps about 68 cents of every sales dollar before other costs

- AI's share: high-performance computing, the category that includes AI chips, made up 66% of revenue

Quick jargon check: gross margin is how much of each sale a company keeps after the direct cost of making its product. A 67.7% gross margin is extraordinarily high and shows how dominant TSMC is. So the business is booming. And yet, the stock slipped. Here's why.

Why a Great-Earnings Stock Can Still Fall

This is the lesson worth remembering. A stock price doesn't reflect how a company did last quarter, it reflects what investors already expected, plus what they think comes next. Three things weighed on TSMC even with record numbers:

1. The good news was already "priced in." When everyone expects a blowout quarter, a blowout quarter is just as expected. Traders call this "buy the rumor, sell the news" the excitement gets bought ahead of time, then some investors take profits when the news actually lands.

2. Worries about spending and margins. TSMC is pouring enormous sums into new factories, including a roughly $100 billion expansion in Arizona. Building cutting-edge plants is hugely expensive, and investors fret that all this capital expenditure ("capex") could squeeze future profit margins, even as sales rise.

3. The mood of the whole market. On the same day, oil prices and tensions in the Middle East had investors selling riskier tech stocks, and TSMC's results "failed to reignite" the AI trade. When the broader market is jittery, even great news struggles to lift a stock. We saw a version of this recently in the chip stock selloff that hit Micron, AMD and Intel.

Why TSMC Is Still a Stock to Watch

A one-day dip doesn't change the big picture, and that's exactly why TSMC belongs on a watchlist. It builds the world's most advanced chips, its customers are the biggest names in tech, and demand for AI processors is still climbing, management pointed to a steep ramp-up of its next-generation 2-nanometer technology (smaller nanometer numbers mean more powerful, efficient chips). With AI-related work already two-thirds of revenue, TSMC is arguably the purest way to follow the entire AI hardware story. For more on how a few chip names drive the market, see our look at AMD's breakout.

The Counter-Argument (And Why It's Serious)

The bear case is real and worth respecting. The biggest concern is geopolitics: most of TSMC's production sits in Taiwan, and tensions between China and Taiwan mean any conflict could disrupt the world's chip supply overnight, a risk no other company carries in quite the same way. On top of that, the heavy spending on new factories could pressure margins for years, chip demand has historically been cyclical (booms followed by busts), and TSMC leans on a handful of giant customers like Apple and Nvidia.

The measured response: TSMC's global expansion Arizona, Japan, Germany, is partly designed to reduce that Taiwan concentration over time, and its technology lead is so wide that customers have few alternatives. The takeaway isn't "ignore the risks" or "back up the truck." It's that TSMC is a high-quality business carrying an unusual geopolitical risk, and both facts are true at once.

The One Number to Watch

Track gross margin. It's currently a remarkable 67.7%, and it's the single figure that tells you whether TSMC's dominance is holding up as it spends billions on new factories. If margins stay high (say, comfortably above 60%) even while capex climbs, it signals the company can grow without giving up its enormous profitability. If margins start slipping quarter after quarter, that's the early warning that the spending is beginning to bite and it's exactly the worry that nudged the stock lower this week. One number, watched over time, tells you most of the story.

Frequently Asked Questions

Why did TSMC stock fall despite record profit?

The strong results were widely expected and already reflected in the price, investors worried that heavy factory spending could pressure future margins, and a jittery market (rising oil and Middle East tensions) pushed people out of tech stocks that day. Good results don't always lift a stock if expectations were already high.

What does TSMC do?

TSMC is the world's largest contract chip manufacturer, or "foundry." It physically produces the chips that companies like Apple, Nvidia, and AMD design, including most of the advanced processors powering artificial intelligence.

Is TSMC a good stock for beginners to watch?

It's one of the most important companies in tech and a clean way to follow the AI-chip story, which makes it worth watching. But it carries real risks especially Taiwan-related geopolitics, so treat it as a stock to understand and monitor, and do your own research rather than acting on headlines.

What is TSMC's biggest risk?

Geopolitical tension around Taiwan, where most of its factories are located. Any serious disruption there would ripple across the entire global technology industry, which is why TSMC is expanding production in the U.S., Japan, and Europe.

Disclaimer: Content on this site is for informational and educational purposes only and does not constitute financial, investment, or trading advice. I am not a licensed financial advisor. Always conduct your own research and consult a licensed professional before making investment decisions.