Nike just handed Wall Street an earnings "beat," and the stock still fell. That contradiction is the whole story. On June 30, the sportswear giant reported fiscal fourth-quarter results that topped estimates on both revenue and profit and shares dropped roughly 4% in after-hours trading before paring some of the loss. The reason is simple once you look past the headline: the profit beat was built largely on a one-time tariff refund, while the part of the business that actually determines Nike's future, Greater China kept shrinking. This post breaks down what Nike really reported, why the market saw through the beat, and the single number that will tell you whether the turnaround is working.

The Headline Beat Was Real But It Wasn't the Business

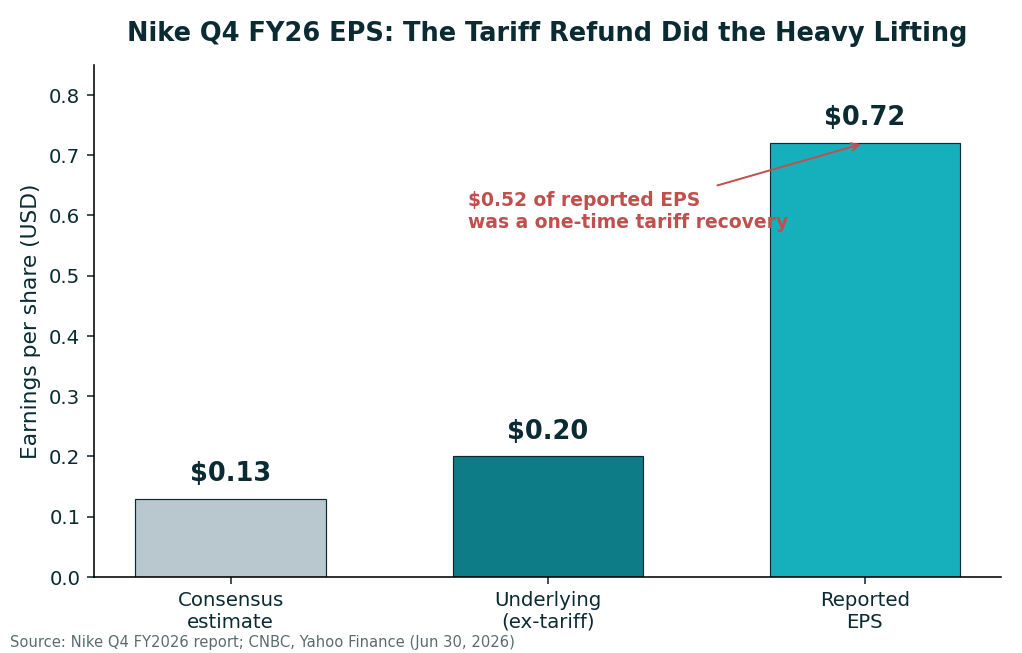

Nike reported fiscal Q4 revenue of about $11.0 billion, down 1% on a reported basis and down 4% currency-neutral. That still came in ahead of what analysts expected. The bigger surprise was on the bottom line: earnings per share landed at $0.72, crushing consensus estimates that clustered around $0.12 to $0.13. On the surface, that looks like a blowout.

Then you read the footnotes. Roughly $0.52 of that $0.72 came from a one-time tariff recovery, a refund of duties Nike had previously paid. Strip it out, and underlying EPS was about $0.20. That is still a beat versus the low-double-digit consensus, so this is not a case of Nike faking its numbers. But there is a world of difference between "we earned $0.72 running the business" and "we earned $0.20 running the business and got a $0.52 tax-and-duty windfall." The market prices the recurring number, not the windfall, which is exactly why the stock didn't celebrate.

China Is the Number That Actually Matters

For most of the last decade, Greater China was Nike's highest-margin growth engine and the region bulls pointed to when justifying a premium valuation. This quarter it did the opposite. Sales in Greater China fell 12% to about $1.30 billion. That is not a rounding error, it is a structural crack in what used to be the most profitable part of the empire.

Management didn't sugarcoat it. Executives signaled that Greater China revenue is likely to keep contracting into fiscal 2027 as the company works through excess inventory, resets pricing, and tries to reposition the brand against aggressive local competitors like Anta and Li-Ning. In other words, the pain in China is not a one-quarter blip that reverses next period; it is a multi-quarter clean-up job that Nike itself is telling you to expect. For a full fiscal year, Nike reported revenue of roughly $46.4 billion, flat on a reported basis, down about 2% currency-neutral with net income near $3.1 billion and diluted EPS of $2.10.

This is the same lesson we've seen play out with other consumer giants navigating leadership and strategy resets. If you want a parallel on how a blue-chip brand's stock behaves during a transition period, it's worth revisiting our breakdown of the Read: Apple CEO change and its impact on Apple stock.

Why the Market Shrugged Off a 'Beat'

Markets are forward-looking discounting machines. They don't reward what already happened; they reprice what is likely to happen next. When a company beats on a non-recurring item but the recurring engine China, in this case, is deteriorating, professional investors mentally subtract the windfall and focus on the trajectory. A 12% regional decline with guidance for more of the same is a trajectory problem, and no tariff refund fixes a trajectory problem.

There is also the quality-of-earnings issue. Sophisticated analysts prize "clean" earnings that come from selling more product at healthy margins. Earnings juiced by refunds, tax items, or asset sales get discounted heavily because they don't repeat. That's why you can beat consensus by a mile and still watch your stock fall the same day: the beat was the wrong kind of beat.

The Counter-Argument (And Why It's Serious)

Here's the strongest bull case, and it deserves a fair hearing. Turnarounds are ugly precisely at the moment they're working. Nike's management is deliberately clearing inventory and resetting China rather than papering over the problem with discounts that destroy the brand long-term. Aggressively taking the pain now, shrinking China revenue on purpose to protect pricing power is what a disciplined operator does before a recovery, not during a collapse. Bulls will also note that revenue beat expectations globally, that the underlying $0.20 still topped consensus, and that a refreshed product pipeline plus a leaner cost base could inflect margins upward once the inventory overhang clears. If you believe the brand's global demand outside China is stabilizing, this quarter is the trough, and troughs are where the best long-term entry points hide.

The measured rebuttal: that thesis rests entirely on China stabilizing on schedule, and management just told you it won't for at least several more quarters. "Trough" calls are only correct in hindsight, and betting on one while the company guides for continued contraction is a bet on management's execution, not on visible improvement in the numbers. The bull case isn't wrong, it's just unproven, and the market rarely pays a premium for unproven turnarounds. Patience here is a position, not a certainty.

The One Number to Watch

Forget the flashy EPS line next quarter. The single number that matters is Greater China revenue growth. As long as it keeps printing negative, that 12% decline to $1.30 billion is your baseline the turnaround remains a story, not a fact. The moment that number stops shrinking and flattens toward zero, then turns positive, is the moment the recovery becomes real and the stock earns the right to re-rate. Everything else, including one-time refunds, is noise. Watch China. It's the tell. For a broader framework on evaluating whether a beaten-down blue chip is a genuine long-term buy, see our Read: guide to judging a long-term buy.

Frequently Asked Questions

Did Nike actually beat earnings expectations?

Yes. Nike reported Q4 EPS of $0.72 versus consensus near $0.12–$0.13, and revenue of about $11.0 billion also topped estimates. But roughly $0.52 of that EPS came from a one-time tariff recovery, so underlying EPS was closer to $0.20.

Why did Nike stock fall despite the beat?

Because the profit beat leaned on a non-recurring tariff refund while Greater China sales fell 12%, and management guided for further China declines into fiscal 2027. Markets discount one-time gains and focus on the deteriorating core, so shares slipped about 4% after hours.

How bad is Nike's China business right now?

Greater China revenue fell 12% to about $1.30 billion in the quarter, and Nike expects continued contraction as it clears inventory and repositions the brand against local rivals. It remains a multi-quarter clean-up rather than a quick rebound.

Is Nike stock a buy after this report?

That depends on your time horizon and risk tolerance. The bull case is a classic turnaround trough; the bear case is that China weakness persists longer than hoped. Watch Greater China revenue growth as the key signal, and do your own research before deciding.

Disclaimer: Content on this site is for informational and educational purposes only and does not constitute financial, investment, or trading advice. I am not a licensed financial advisor. Always conduct your own research and consult a licensed professional before making investment decisions.