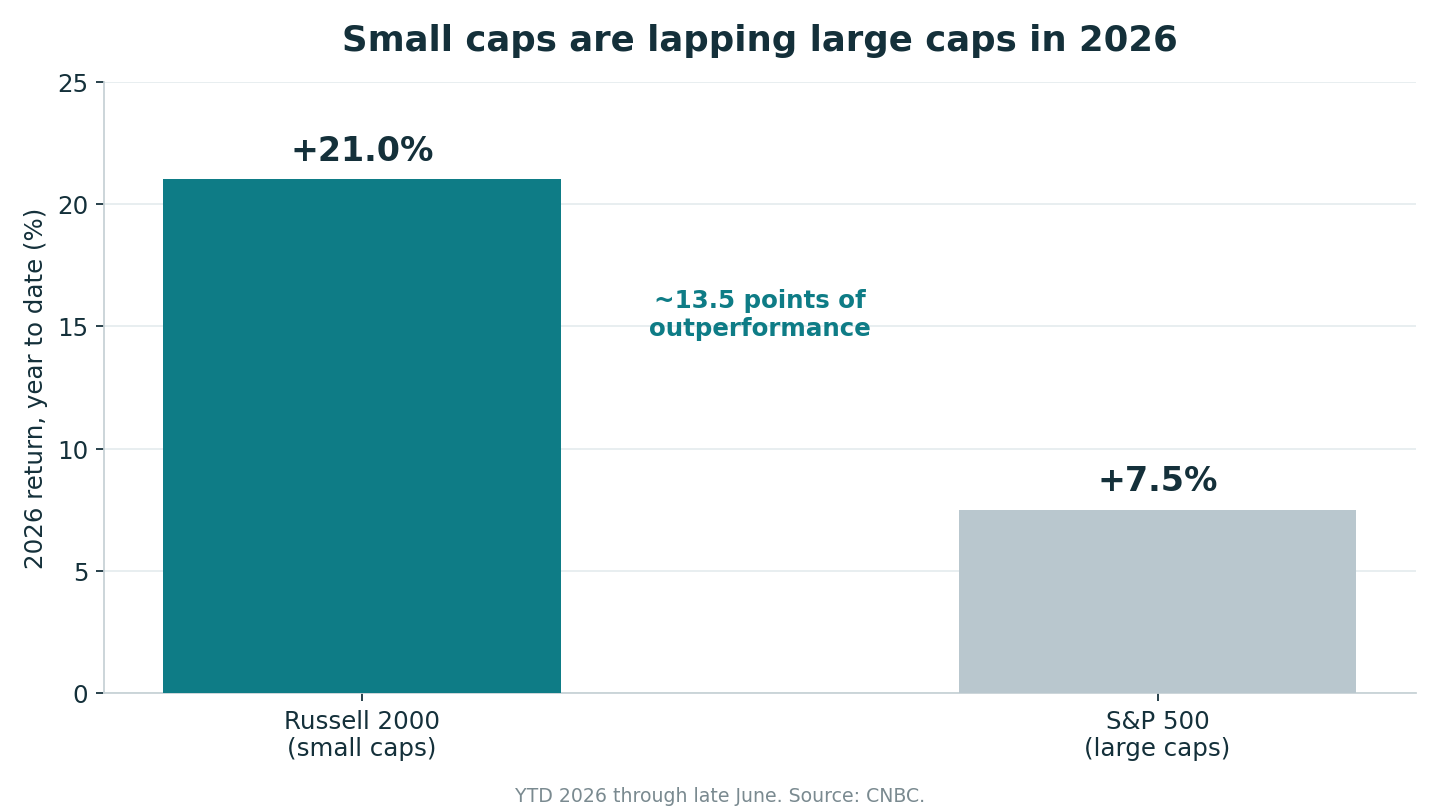

For three years the market had one story: a handful of mega-cap names carried everything, and everyone else waited. That story just broke. The Russell 2000 is up roughly 21% in 2026 and touched an all-time high near 3,034 — its best first half since 1991. Meanwhile the S&P 500 has managed about 7.5%. Small caps aren't just participating in the rally anymore; they're lapping the giants. The question that actually matters for your portfolio isn't whether it happened. It's whether it lasts.

The Rotation Is Broader Than One AI Trade

The easy explanation is "AI spread out," and it's partly right, but the mechanics are more interesting than the headline. The AI infrastructure build-out has stopped being a story about three chip designers and started being a story about their suppliers: test-equipment makers, specialty component firms, and second-tier fabricators that small-cap indexes are full of. Chip-related names account for 16 of the Russell 2000's 50 best-performing stocks this year, and a few Aehr Test Systems, Ichor Holdings, MaxLinear, have rallied more than 400%.

That breadth shows up in the fundamentals, not just the tape. Consensus 2026 earnings-growth forecasts for Russell 2000 companies have climbed to about 38%, up from roughly 23% at the start of the year. When analysts revise a whole index's earnings up by 15 points in six months, that's not a sentiment blip, that's the market re-underwriting what these companies are worth.

Read: Micron's HBM Supercycle Could Redefine AI Growth

The Real Engine Is the Fed, Not the Hype

Here's the part the AI narrative under-sells. Small caps are far more leveraged literally, than large caps, and they borrow differently. Roughly 40% of Russell 2000 debt is floating-rate, versus under 10% for the S&P 500, whose members mostly locked in cheap long-term fixed rates years ago. So when the Fed delivered three consecutive quarter-point cuts in late 2025, dragging the funds rate to 3.50–3.75%, it wasn't a vibe. It was an immediate cut to interest expense that flows straight to the bottom line of thousands of smaller companies.

That's the structural piece: small-cap earnings are geared to the rate cycle in a way the S&P 500 simply isn't. Falling rates don't just lift valuations, they mechanically improve small-cap cash flow. Which is exactly why the same dynamic is the bear case in disguise.

The Counter-Argument (And Why It's Serious This Time)

Every small-cap breakout of the last decade has been a head-fake. 2016, 2021, early 2024, each time small caps "finally" took leadership, and each time large caps reclaimed it within a couple of quarters. Why believe 2026 is different? Three honest reasons for caution:

First, the leverage cuts both ways. That floating-rate debt is a tailwind while the Fed eases, and a trap the moment it stops. If inflation data forces the Fed to pause or reverse, the same balance sheets that just got a liquidity injection get squeezed. A rotation built on rate cuts is only as durable as the rate cuts.

Second, quality. The Russell 2000 still contains a large share of unprofitable companies, and a rally that lifts the profitable and unprofitable alike tends to unwind indiscriminately when risk appetite fades. Some of this year's 400% names are riding momentum, not durable moats.

Third, concentration risk from this year's Russell reconstitution has drawn explicit warnings from strategists at Morgan Stanley, who note the reshuffle blurred style lines and pushed more of the index's weight into fewer, larger "small caps." An index that's increasingly top-heavy behaves less like the diversified small-cap exposure investors think they're buying.

Read: 3 AI and Tech Stocks to Watch in 2026

The bull rebuttal is that this time the leadership is backed by real earnings revisions and a genuine easing cycle, not just hope, and Goldman Sachs has pointed out that if the 1,240-basis-point outperformance holds, it would be the largest year of small-cap outperformance since 2003. But 2003 is a double-edged reference: it was the start of a durable run and a reminder that these regimes begin from deeply washed-out valuations. The setup rhymes; it doesn't guarantee.

The One Number to Watch: The Payrolls-to-Fed Feedback Loop

Forget the index level. Watch the labor data and what it does to rate expectations. June nonfarm payrolls land this week, and every print from here feeds directly into whether the Fed keeps cutting. Strong-but-not-hot jobs data is the perfect regime for small caps: enough growth to justify the earnings upgrades, soft enough to keep cuts on the table. A hot number that pushes cuts off the table is the single fastest way to end this rotation. If you own small-cap exposure, the jobs report is now more important to you than any earnings call.

FAQ

Q: Why are small caps up 21% while the S&P 500 is up only 7.5%?

Two engines running at once: the AI build-out spreading to smaller suppliers, and Fed rate cuts that disproportionately help small caps because 40% of them carry floating-rate debt.

Q: Is this a bubble?

Not obviously, the rally is backed by real earnings-growth upgrades (from 23% to 38% for 2026). The risk isn't valuation froth so much as dependence on the Fed continuing to cut.

Q: What kills this rotation?

Hot inflation or jobs data that forces the Fed to pause. The same floating-rate leverage that's a tailwind today becomes a headwind the moment easing stops.

Q: How do I get exposure without picking single names?

Broad small-cap index funds or ETFs (like ones tracking the Russell 2000) give diversified exposure, though note this year's reconstitution has made the index somewhat more top-heavy than in the past.

Disclaimer: Content on this site is for informational and educational purposes only and does not constitute financial, investment, or trading advice. I am not a licensed financial advisor. Always conduct your own research and consult a licensed professional before making investment decisions.