Advanced Micro Devices just did something it had never done before: closed at a record high with a market cap knocking on $950 billion. The instinct is to file it under "the AI trade" and move on. That would be a mistake. AMD's July 1 breakout up 7.7% to about $581, its highest close ever wasn't really about GPUs at all. It was about the least glamorous corner of the business: server CPUs. And that's exactly why it may prove more durable than the hype suggests.

The Breakout Is a Server-CPU Story, Not a GPU Story

Peel back the catalyst and you find a chip that never gets magazine covers: EPYC. AMD confirmed that its 6th-generation, 2nm "Venice" server processors have entered their production ramp, with volume scaling through the second half of 2026 and, crucially, more customers validating and ramping Venice than any prior EPYC generation. A five-star Wells Fargo analyst raised his price target on the back of a meaningful upward revision to server-CPU revenue estimates, not accelerators. The data-center segment already did $5.78 billion in a single quarter, up 57% year over year, with management guiding the next quarter to roughly $11.2 billion in total revenue, implying about 46% growth. When the "boring" business compounds at that rate, the whole stock re-rates.

This matters because CPU share is stickier than GPU mindshare. Every point of server-CPU share AMD takes from Intel is a multi-year annuity data-center operators standardize on a platform and don't rip it out the next quarter.

The AI Accelerator Upside Is the Option, Not the Thesis

None of this means the AI story is fake. AMD said customer engagement around its MI450 series and "Helios" rack-scale systems is strengthening, with leading-customer forecasts running ahead of initial expectations, and the MI400-series roadmap is intact. But notice the framing: the accelerators are the upside option on top of a CPU base case that already justifies the move. Buy AMD purely as an "Nvidia alternative" and you are underwriting the hardest, most competitive part of the story. Buy the CPU franchise and you get the AI optionality thrown in.

Read: Micron's HBM Supercycle Could Redefine AI Growth

The Counter-Argument (And Why It's Serious)

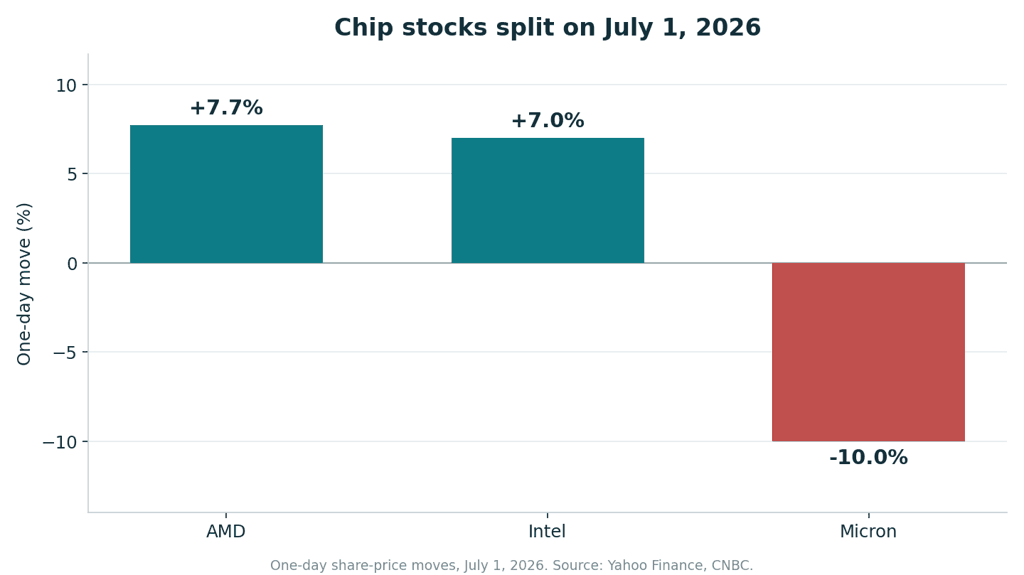

Here is the strongest bear case. At roughly $950 billion, AMD is priced for a lot to go right. Nvidia still owns the AI-accelerator market by a wide margin, and its CUDA software moat has humbled every challenger so far. Semiconductors also reprice violently: on the very same day AMD popped, Micron fell more than 10% as investors took profits on chip names that had run up around 80% in the first half — a reminder of how fast sentiment turns. And Intel is not a corpse; a credible product response or aggressive pricing could slow AMD's share gains and compress margins.

The rebuttal is that AMD's re-rating is anchored to revenue and share data already showing up in results, not to a promise. But "already in the numbers" cuts both ways: expectations are now high, and any stumble in the Venice ramp or MI450 qualification would be punished quickly.

Read: 3 AI and Tech Stocks to Watch in 2026

The One Number to Watch: The EPYC Venice Ramp

Forget the daily tape. The tell is Venice. If AMD's 2nm server CPUs ramp on schedule through the second half of 2026 and the customer count keeps climbing, the data-center CPU share story stays intact and the stock's premium is defensible. If the ramp slips or Intel claws back share, the "it's not about GPUs" thesis loses its floor — and a $950 billion valuation gets much harder to defend. Watch the next two earnings calls for Venice volume commentary; that is the number that matters.

FAQ

Q: Why did AMD stock jump on July 1, 2026?

It hit a record high near $581 (+7.7%) after a Wells Fargo price-target increase driven by higher server-CPU revenue estimates and the 2nm "Venice" EPYC ramp, not primarily GPUs.

Q: Is AMD's rally just the AI trade?

No. The immediate catalyst was the EPYC server-CPU business. The MI450/Helios AI accelerators are upside optionality on top of that, not the base case.

Q: What's the biggest risk?

A rich ~$950B valuation, Nvidia's entrenched CUDA moat, and how violently chip stocks swing, Micron fell more than 10% the same day AMD rallied.

Q: What should investors watch next?

The 2nm "Venice" EPYC production ramp and customer count through the second half of 2026.

Disclaimer: Content on this site is for informational and educational purposes only and does not constitute financial, investment, or trading advice. I am not a licensed financial advisor. Always conduct your own research and consult a licensed professional before making investment decisions.